Venture Geopolitics Issue 19

28 October 2025

Finance is quietly automating itself. OpenAI’s “Project Mercury” has bankers training their own replacements – teaching models the judgement (and formatting) of corporate finance. At the same time, Polymarket is raising at a $12–15B valuation, as investors experiment with pricing probability rather than risk. Financial markets are chasing predictability even as their foundations grow opaque: the collapses of First Brands & Tricolor, and the Bank of England’s warning on private credit as a “canary in the coal mine”, hint at potential fragility.

As finance automates and volatility becomes ambient, power is shifting elsewhere. Europe is redrawing its industrial map – Airbus, Leonardo and Thales merging their space divisions into a €6.5bn sovereignty venture; the UK pushing a “Steel Alliance” with the US and EU; and Synthesia rejecting a $3B bid from Adobe to stay independent – a rare show of European resolve!

Beneath it all, the world is reorganising around autonomy – of capital, computation and production.

IPOs / Public

US govt shutdown still freezing IPO market – just 5 small IPOs and 4 SPACs last week as backlog drags on.

Navan (corporate travel platform) set to raise $923M in one of the year’s biggest VC-backed listings, rumoured for Oct 30 (here)

KR1 (Isle of Man-based crypto staking firm), will shift from Aquis Exchange to LSE main market – first such move in years, signalling growing regulatory comfort with crypto listings in UK (here)

London Stock Exchange Group collab with Anthropic to integrate LSE data into Claude via its Financial Analytics products. Part of LSEG Everywhere AI strategy, which aims to embed AI across platforms to enhance financial decision-making (here)

Reddit (online discussion and social news platform) sued Perplexity (AI powered search) and three data-scraping firms, accusing them of illegally harvesting its content to train Perplexity’s search engine. Case adds to growing copyright battles between AI firms and content owners (FT)

Qualcomm (mobile chip and wireless tech) shares jumped 20% after unveiling its first AI data-centre chips, directly challenging Nvidia. Saudi Arabia’s Humain (PIF-backed) will be first to deploy, with 200MW of capacity planned for 2026 (here)

More generally in public markets…daily share price swings worth hundreds of billions have become routine this year, with individual stocks gaining or losing over $100B 119 times - mainly Microsoft, Apple, and Nvidia. Bank of America says 2025 already exceeds 2024 in market “fragility events.” Recent offsetting moves across them have kept volatility low - but if they move together, risks could rise. Meta, Alphabet, Microsoft, Apple, and Amazon reporting this week (FT)

Big Dogs

OpenAI launched ChatGPT Atlas, a new AI-powered web browser that integrates ChatGPT into every aspect of online browsing. Atlas lets users “Ask ChatGPT” directly while browsing. The move challenges Google’s dominance (≈90% search, 70% Chrome) and coincided with Microsoft unveiling a similar AI-native browser (here)

OpenAI hired >100 former bankers from Goldman Sachs, JPMorgan, and Morgan Stanley to train AI for advanced financial modelling (“Project Mercury”). Paid ~$150/hour, participants help the system learn tasks such as IPO, LBO, and restructuring analyses. Per Matt Levine: “what you want… is to take an AI chatbot and have an investment banking vice president yell at it for a few years until it gets the formatting right - ‘reinforcement learning,’ I believe this is called.” The effort underscores OpenAI’s broader enterprise push and deepening ties with Wall Street, following a $4B credit facility from JPMorgan (here)

Anthropic (AI research and safety) has struck a multi-billion-dollar deal with Google Cloud to access up to one million TPUs and more than one GW of compute capacity by 2026, deepening their partnership and escalating the AI infrastructure arms race (here)

Polymarket (prediction platform) reportedly raising at a $12–15B valuation (>10x its worth just four months ago after backing from Peter Thiel’s Founders Fund). Momentum around prediction markets accelerating (Coindesk). Great analysis from Karim Al-Mansour exploring how these “markets for reality” could transform global finance by pricing uncertainty itself, even as liquidity, legal, and regulatory frictions keep them on the fringe of institutional adoption.

Synthesia (AI video platform) rejected $3B takeover bid from Adobe choosing independence and a future IPO. A rare case of European founders saying no to US acquisition! (Sifted)

Crusoe Energy (AI infra & datacentres) raised $1.4B (led by Mubadala, Valor) at $10B, funding a 1.8GW campus in Wyoming and gas-powered sites in Canada (here)

Redwood Materials (energy-storage & battery-recycling company) raised $350M at $6B+, led by Eclipse Ventures with a strategic investment from Nvidia (Techcrunch)

Uniphore (enterprise AI platform) raised $260M at $2.5B, led by Nvidia, AMD, Snowflake, and Databricks – a rare cross-chip alliance backing enterprise AI (here)

Sesame (voice-AI & hardware startup) raised $250M after its AI voices Maya and Miles hit 5M+ minutes of conversation. Building smart glasses to carry personal AI assistants - a market no Big Tech player has yet cracked (Techcrunch)

Mercor (AI training marketplace) confirmed a $350M round at $10B (led by Felicis, joined by Benchmark, GC, Robinhood Ventures). Connects experts to AI firms for model tuning - generating $1.5M+ daily revenue (here)

Venture Capital

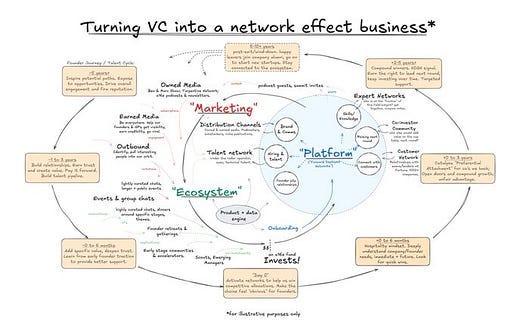

a16z raising $10B across new vehicles - $6B for growth, $1.5B each for AI apps and AI infra, plus $1B for “American Dynamism”. Firm’s strategy: convert its vast founder network into enduring infrastructure - a compounding model reshaping venture itself. See diagram below (and here and here).

Nelson Peltz’s Trian Fund and VC fund General Catalyst have jointly offered $7bn to take Janus Henderson private. GC, now managing $40B+ and fresh off an $8B 2024 raise, argues VC must move beyond one-size equity to custom capital. This “scale-and-structure” shift underpins GC’s thesis that Janus Henderson can modernise faster outside public markets (here)

Lakestar will now focus solely on existing portfolio companies and supporting his team in spinning out new ventures or funds, not launching new vehicles. Hasn’t ruled out involvement in resilience sectors, though (defence, security, supply chains) - Hommels reiterated his belief that Europe must build industrial champions, not just unicorns (FT)

2 metrics defining VC: Burn Multiple (cash burned ÷ net new ARR) and BEI (revenue per $ raised) (DataDrivenVC)

o Benchmarks are clearer than ever: burn <1.5x = excellent; 1.5–2.5x = average; >2.5x = red flag. BEI >1.0x (>$1 ARR per $1 raised) is elite. Series A firms should aim for ~1.2x burn or better.

o Raising an A now takes 2+ years, with only ~20% of startups succeeding. Expect to show $2–3M ARR and ~3x YoY growth; $3M is the new bar. Median AI startups hit $1M ARR in ~11 months (vs 15 for SaaS) and $5M in ~2 years.

o Takeaway: show $2M ARR on $1M burned or $5M ARR from $3M raised – proof of real demand and disciplined execution.

Coatue’s Public Markets presentation frames the current AI-driven investment cycle as a structural transformation rather than a speculative bubble. Their analysis of 30+ historical bubbles over 400 years suggests that while 1/3 of the current AI trade may be frothy (“AI reckoning”), roughly 2/3 reflects genuine value creation (“AI abundance”). Crucially, AI capex is being funded through operating cash flow, not leverage — a sharp contrast with the dot-com era. Coatue also notes that market multiples remain well below 2000-era extremes, supporting their view that we’re still in the build-out phase of a durable cycle. They warn that “selling early” can be costly in long secular growth waves (here)

Venture Geopolitics

Airbus, Leonardo and Thales have agreed to merge major parts of their satellite and space-systems divisions into a single entity, employing about 25k people and generating roughly €6.5B annual revenue by 2027. The venture focusses on satellite manufacturing, secure communications, and defence-grade space services. Politically, it is a sovereignty project: Europe’s answer to U.S. dominance by SpaceX and Amazon’s Kuiper, designed to underpin EU programmes like IRIS, which seek autonomous, encrypted satellite networks for governments and critical infrastructure (Guardian)

UK pushes “Steel Alliance” with US and EU aiming to counter global overproduction, especially China’s 1B-tonne output. Trade minister Sir Chris Bryant called steel essential to “economic security … for building tanks and all the rest of it.” With Scunthorpe now the UK’s only active blast-furnace, the goal is a “ring of steel” to secure jobs, deter cheap imports, and preserve industrial sovereignty (FT)

President Trump and PM Takaichi (Japan’s new and first female PM) pledged a “new golden age” of cooperation, linking security with economic strategy. The pact targets joint control of rare earths and critical minerals, reduced dependence on China, and tighter defence-industrial integration. It exemplifies venture geopolitics in action – state capital and investment policy deployed to shape supply-chain power (FT)

Following the bankruptcies of First Brands & Tricolor, Matt Levine notes how risk in credit markets hasn’t vanished, only migrated. Post-2008, regulation drove risky lending from banks to non-depository financial institutions (NDFIs) such as private-credit funds. Banks now lend to the lenders, moving “up the capital structure” to safer-looking positions – but with “more seniority, less visibility.” US bank exposure to NDFIs has hit $1.2T, creating diversification with opacity (Bloomberg)

Meanwhile, governor of Bank of England warned recent events in US private credit markets have echoes of sub-prime mortgage crisis. Appearing before House of Lords committee, he said it was important to have the “drains up” and analyse the collapse of two leveraged US firms, First Brands and Tricolor, in case they were not isolated events but “the canary in the coalmine” (The Guardian)

Trump administration is weighing equity stakes in quantum-computing firms (IonQ, Rigetti, Atom Computing) in exchange for federal funding. As with state-of-the-art chips, Trump views advancements in quantum computing as integral to US national security (WSJ)

European Commission will propose the EU’s “28th regime” for startups as a directive rather than a regulation, according to a leaked 2026 work programme. This approach has triggered backlash from EU–INC and startup associations who argue that only a regulation can truly eliminate barriers to scaling European startups. The final proposal by the Commission is expected in Q1’2026 (Euractiv)

The EU’s proposed Corporate Sustainability Due Diligence Directive (CSDDD) would make large firms, including non-EU ones earning >€450mn in Europe, responsible for ensuring supply chains do not harm people or planet, with fines of up to 5% of global turnover. In a joint letter to EU leaders, the US and Qatar called the law an “existential threat” to Europe’s economy - warning it could block vital LNG supplies as the EU aims to end reliance on Russian gas by 2027 (FT)

Canada fast-tracks Port of Montreal expansion under its new Major Projects Office to bypass US chokepoints and boost trade with Europe, MENA, and South Asia. The move aims to insulate exports from US–China trade tensions and marks a wider shift toward infrastructure-led economic sovereignty (WSJ)

UK Government pledged £500M for the Oxbridge corridor, including £400M for Cambridge infrastructure, aiming to add £78B to GDP by 2035 (BBC)

Strategic Sectors

AI

China’s DeepSeek is winning vs OpenAI and Google in Africa (Bloomberg)

Chinese startup MiniMax AI has released MiniMax-M2, a 230B-parameter open-source language model using a “Mixture-of-Experts” design that activates only 10B parameters per task, delivering frontier-level performance at far lower compute cost (it claims costs 8% as much as Claude’s current Sonnet model and is twice as quick). Licensed under MIT, M2 enables full commercial deployment (VentureBeat)

Dealroom’s Global Tech Ecosystem Index ranks Paris as the world’s #3 AI hub, behind the Bay Area and New York. The city hosts 500 AI startups (63% of France’s total), 150 research centres, and 111k trained workers. Open-source leaders Mistral AI ($2.9B raised) and Hugging Face anchor its ecosystem. Paris even surpasses Silicon Valley in early-stage alumni founders (1,380 vs 1,146). The report also spotlights rising frontier-AI momentum across MENA, signalling a more multipolar global landscape for innovation (here)

Noah Smith argues that the much-hyped “circular” AI deals aren’t shady accounting (or round tripping) but a form of vendor financing that ironically diversifies risk. Nvidia, for instance, gets over half its revenue from just four major customers, leaving it exposed if any one falters. By striking deals with newer players like OpenAI and AMD, Nvidia isn’t escaping its dependence on AI, but it is spreading that dependence across more partners—an odd kind of safety in shared risk. If AI as a whole collapses, everyone goes down together, but at least no single company can take Nvidia with it (here)

{kind=link}

Robotics

Amazon announced plans to cut up to 30K corporate jobs (c.10% of its office workforce) while also reducing future hiring through automation. Documents leaked to the NY Times reveal ambitions to automate up to 75% of operations by 2027, potentially avoiding the need to hire 160K additional U.S. workers and replacing over 500K human roles long-term (Reuters, NY Times)

Cybersecurity

Veeam announced a $1.73B acquisition of SecuritiAI, aiming to merge backup/disaster-recovery with data discovery, privacy, and data security posture management (here).

Crypto

Revolut has become one of the first firms in Europe to gain approval under the EU’s new MiCA crypto rules, allowing it to offer digital currencies across 30 countries in a fully regulated way. Already a licensed bank, Revolut can now link traditional finance with crypto more safely and transparently, letting customers move between money and digital assets without hidden fees. It’s a major step towards Europe’s first truly regulated “crypto bank” and a sign that digital finance is entering the mainstream. The news comes in the same week reports emerged of a foiled plot to kidnap Revolut’s CEO, Nikolay Storonsky (Coindesk, Reuters)

A16z annual State of Crypto report showcases crypto growing up. Significant institutional adoption (Visa, BlackRock, Fidelity, JPM, PayPal, Stripe) and blockchain transaction growth of >100x in last 5years. Stablecoins power $46T ($9T adjusted) in annual transactions, in the leagues of Visa & PayPal. >$175B sits in Bitcoin and Ethereum ETF products. On chain activity growing fastest in developing countries. (monthly active crypto users grown to 40-70M and there are 716M crypto owners). Stablecoins now rival worlds largest payment networks in transaction volume (ACH, Visa) and are already a top 20 holder of US treasuries – ahead of Saudi Arabia, South Korea, Germany and Israel (a16z)

Energy/Climate

TotalEnergies was found guilty by a French court of law of having misled consumers with claims about its contributions to tackling climate change (Guardian)